Day, welcome to Home Biz Tax Talk. My name is Lissandra Everett, and I am the Home Biz Tax lady. I help home business owners win the tax game. Home Biz Tax Talk airs Monday through Friday at 9:00 o'clock ish. When you tune into my show, you're gonna hear about topics that are important to the home business community. Alright, today we're focused on healthcare. I got a question about whether the healthcare mandate or penalty has been removed for plans starting in 2019. So, when you file taxes in 2020, there will be no penalty. However, for taxes being filed in 2019 and previously, when the Affordable Care Act was enacted, there will be a penalty. If you did not have healthcare for the 2018 year and you're filing your taxes in 2019, there will be a penalty. Now, there have been some changes to healthcare. I don't sell health insurance, but I research it so I can give you some information to think about and questions to ask professionals in that field. Starting in 2019, there are these things called catastrophic plans. It's important to go and read about them, especially when I'm seeing medical bills for ninety-eight thousand dollars for one month. That is just crazy. One thing I've been hearing is that people are opting out of healthcare. Even if you make that choice, you still need to set aside money and think about your healthcare. The fact is, you may still need to go to the doctor, get a physical, or in case of an accident, you still need to be able to care for yourself. I had a conversation with a young man in his late 20s or early 30s, and he was unsure about healthcare. I asked him, "If you go out here and get...

Award-winning PDF software

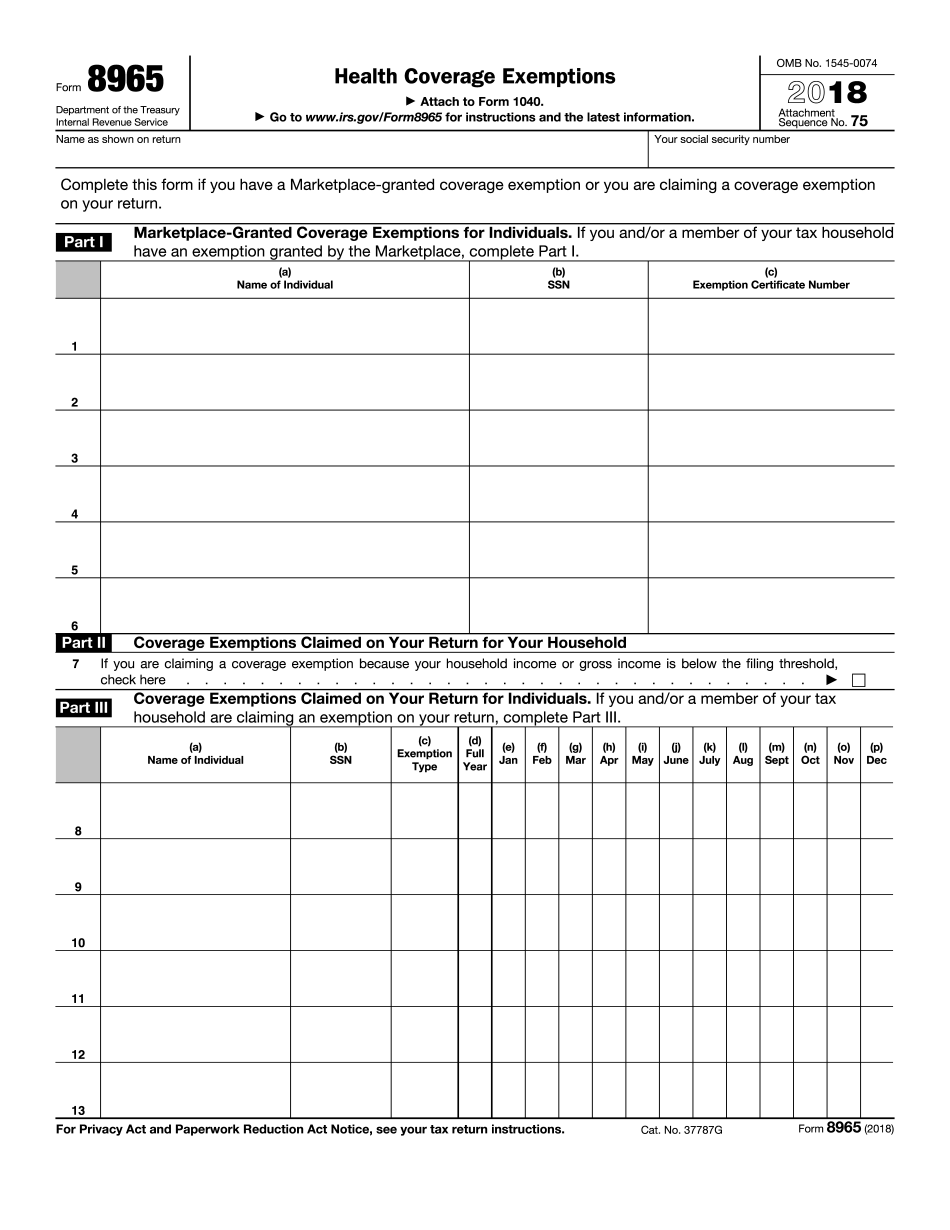

Health coverage exemptions Form: What You Should Know

Use the Form 8965, Health Coverage Exemptions, to claim an exemption for yourself from having to pay the Medicare taxes due on Medicare premiums; pay the premium tax on a premium health plan that you receive from an employer; or pay an employer's share of a qualified health plan, to the extent that your coverage is qualified through an Exchange. Note: For tax year 2025 or earlier (see the following for exceptions), you should: 1) Use Form 8965, Health Coverage Exemptions (Form 8965-SS), to claim an exemption for yourself from having to pay a tax due for being uninsured. 2) Use Form 8965-SS or a copy of your claim from Form 8965-SS to include with your return on which you make payment for not having health insurance. It is recommended that you complete both forms. See the text below for information about if one form is required and how to file for and claim an exemption. 1) If you did not file Form 8965-SS for the prior Tax Year If, under IRS guidance, you will not claim an exemption for yourself from making payments for not having health insurance, you will need to file Form 8965, Health Coverage Exemptions (Form 8965-SS), to complete tax returns. 2) If you used Forms 1099-R, W2G or W2HS to calculate Health coverage exemptions for both Tax Years 2025 and 2017, only the following information may be on Forms 8965-SS: Tax ID Number; 2) This form does not need to be completed and sent to you if you have already filed and sent Forms 8965 for both Tax Years. 3) This form must be completed and sent to you if you received a health coverage exemption for the 2025 tax year, but you did not file Form 8965 for the 2025 tax year. 4) This form must be completed and sent to you, or if filing a joint return for 2017, with the completed Forms 8965 for both tax years. If you filed Forms 8965 for both Tax Years, you will need to complete this form for each of them.

online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do Form 8965, steer clear of blunders along with furnish it in a timely manner:

How to complete any Form 8965 online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your Form 8965 by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your Form 8965 from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.

Video instructions and help with filling out and completing Health coverage exemptions